NAIOP – Mid-Year Market Round Up June 2015

By Bruce Lee

The 2015 NAIOP Mid-year summary meeting was very well attended – over 400 in the audience including myself and Grey Lee representing Lee Partners. The esteemed panel of real estate professionals gave a current market “snapshot” of their market area of expertise.

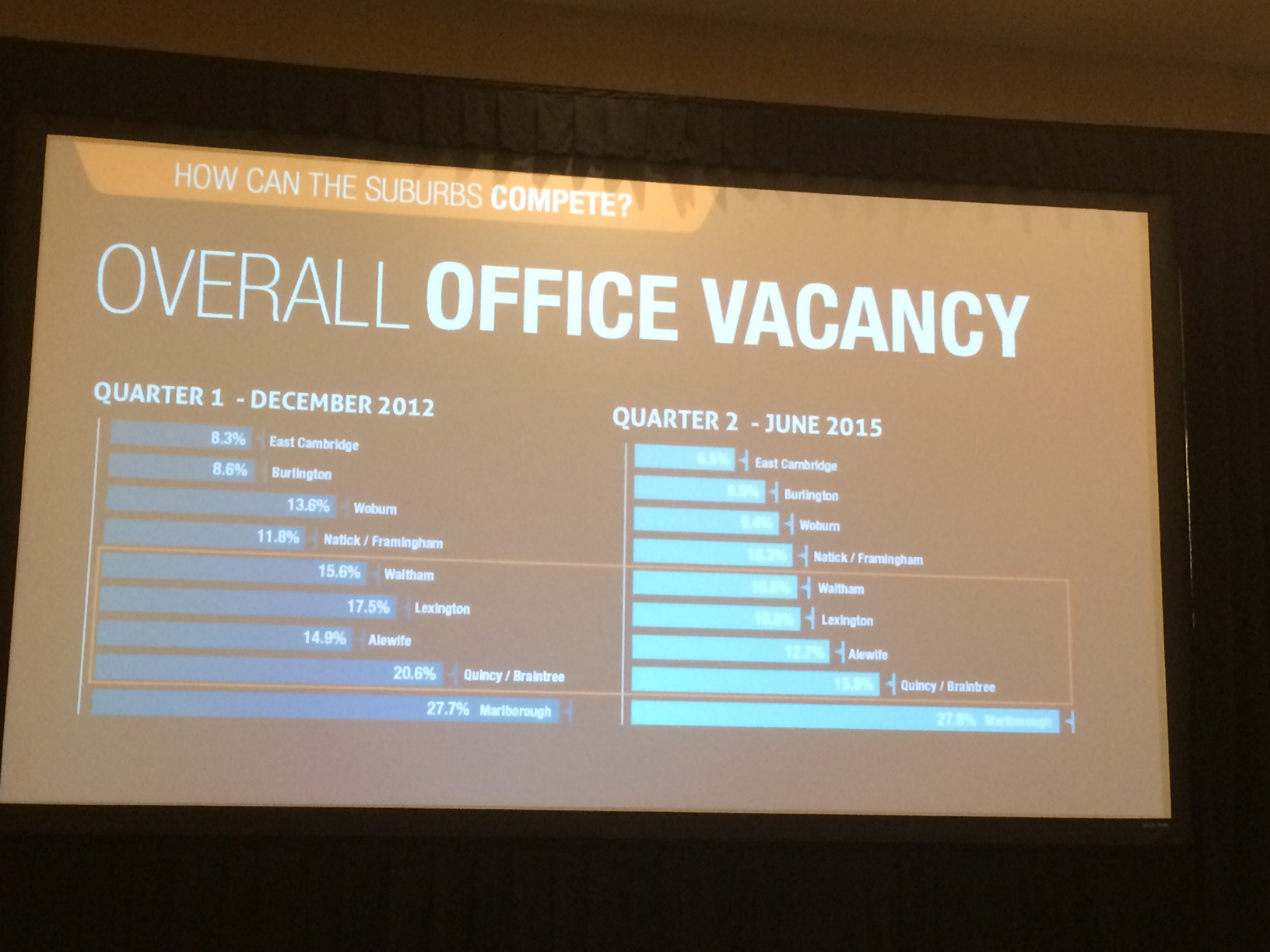

Hans Nordby, Managing Director of CoStar Portfolio Strategy led off the panel review – providing a snapshot of the Boston economy and its impact on the local real estate market. The good news shared by Hans is that Leading Economic Indicators are strong and he expects them to continue to grow at a 3% rate for 2016. Tech job growth is projected to be at a 2.8% rate. In addition, Boston is experiencing very strong growth in it public transportation in-bound traffic from the suburbs – despite a mass transit system that is aging. Large and expensive buildings are going up and building sales are booming. Cap rates have compressed into the 3 to 4 range with one building trading at a 3.1 cap rate. Boston office vacancy is now at the same as it was in 2007 and it will get tighter as Tenant demand is strong. For buildings built between 2000 and 2007 the vacancy rate is now at 1.5%. Almost all new space under construction is pre-leased. Suburban office space built in the 90’s is doing well and space built pre 1980’s is doing OK. The lagging sector of the suburban office market is buildings built in the 1980’s. Eleven percent of this space is vacant – representing 18 million sq. ft. These buildings have large floor plates, many difficult to sub-divide, located away from amenities with narrow windows. 40 % of route 128 office leasing in the last 5 years has been concentrated in two towns – Waltham and Burlington.

Andrea DeSimone of CBRE Retail then spoke to the local retail market – characterizing retail as “re-invention” where retailers are rolling out new concepts for the new stores – including Macy’s , Koll, Whole Foods, Roche Brothers, Walgreens, Target and CVS. Many food retailers are expanding in this area – Wegmans, Whole foods, H market & Star Market are rolling out new store concepts. In addition, food emporiums / eateries are entering the area – including Todd English, Le District, and Chelsea Market. Babbo – most expanding from New York City.

Duncan Graton from DTZ discussed the suburban office market – Duncan recommended that owners of suburban office buildings take aggressive action to reposition their offerings to compete – to include (1) renovating the Atrium and having walk able amenities close by (2) teaming up with restaurants for Tenant food services instead of cafeterias (3) Make sure lots of “bar stools” are nearby (amenity rich areas) – Clarks recently before leasing 1275 Main Street in Waltham wanted to know as part of their leasing requirement – how many bar stools were within walking distance or nearby (1265 Main had 195!) (4) Bike friendly support areas (5) pet friendly spaces and car chargers and outside garden areas. For transportation – more bus services are coming – provided by private companies and developers due to minimal public infrastructure transportation support for office tenants in the suburbs. Tenants want a younger labor force. Some notable tenants have moved back into the Boston market -i.e. AutoDesk from Waltham and now all the VC’s that moved to Waltham a decade ago are back in Cambridge/Boston. Duncan shared a few new renovation examples – one being 170 Tracer Lane in Waltham – where a 1980’s red brick ribboned windowed building is being totally re-skinned in glass. This represents the future of suburban office product – mostly glass exteriors where Tenants can share natural light and walk to amenities – in this case Reservoir Place next door. Improved glass technology that also insulates and is energy efficient is allowing this transformation.

John Olsten of JLL discussed the Cambridge Market – Class A office space in now leasing the $60’s to $70’s per sq ft – when you can find it. Although this may seem to be a high lease rate – it is much lower than in the San Francisco Bay area and national west coast tenants continue to expand in the Cambridge area. Cambridge lab space has a vacancy rate of 3.5%. So, it is not a question of what space costs in the Cambridge Kendall Square area – expanding office and tenants have very few local alternatives to consider.

Ron Perry President of Boston’s Colliers office – Landlords are “riding the wave” and enjoying four straight years of positive absorption – 1.3 million square feet each year. This year absorption is positive by 675,000 sq ft. The Boston vacancy rate has declined from 16% to 10%. The market consists for 63 million sq ft of office space with the average asking lease rate now $49. This current rate is 50% higher than 10 years ago. Asking lease rates for new construction range from $35 to $85 per sq ft. The Seaport district average rent is $46 with a 15% vacancy rate. Class A space in low rise Boston buildings now leases in the $40 range. Going forward Ron expects rents to increase at 5 to 10 percent per year for at least the next few years.

Lauren O’Neil with HFF discussed Capital Markets – Boston is now the second most favored city in the USA for foreign investment in Real Estate Assets. The market is very strong with buildings trading at 3.7 to 3.9 cap rates. Bidding wars over trophy buildings are common. An additional comment Lauren made was that new construction costs in Boston are the same as in New York City – but rents in Boston are much lower.

Summary: Commercial property owners in the Boston area are well position to benefit from this rising market that is expected to continue for at least a few more years. Tenants that are renewing long term leases can expect much higher lease rates on a renewal basis or on a relocation into a similar type building. Offsetting this difficult tenant leasing environment is the benefits provided by mobile technologies that allow for more off-site working productivity and less need for individual in-house office space. Shared office space, smaller cubicles and even desks without the need for file space will allow for increased employee density and lower overall office/facility cost per employee – even in a rising office lease rate environment.